Think of Crypto Like a Toy You Bought

Imagine you buy a toy for ₦10,000. Later you sell it for ₦25,000. You made ₦15,000 profit. The government says, “Nice! Pay tax on that profit.” Crypto works the same way. The government now treats Bitcoin, Ethereum, USDT, NFTs, and other digital coins like property or assets.

From 2026, Nigeria has clearer rules under the new tax laws. Profits from crypto are taxable. Exchanges must link your transactions to your TIN (Tax Identification Number) and NIN (National ID). They report data to the Nigeria Revenue Service. The blockchain is public, so hiding is very hard.

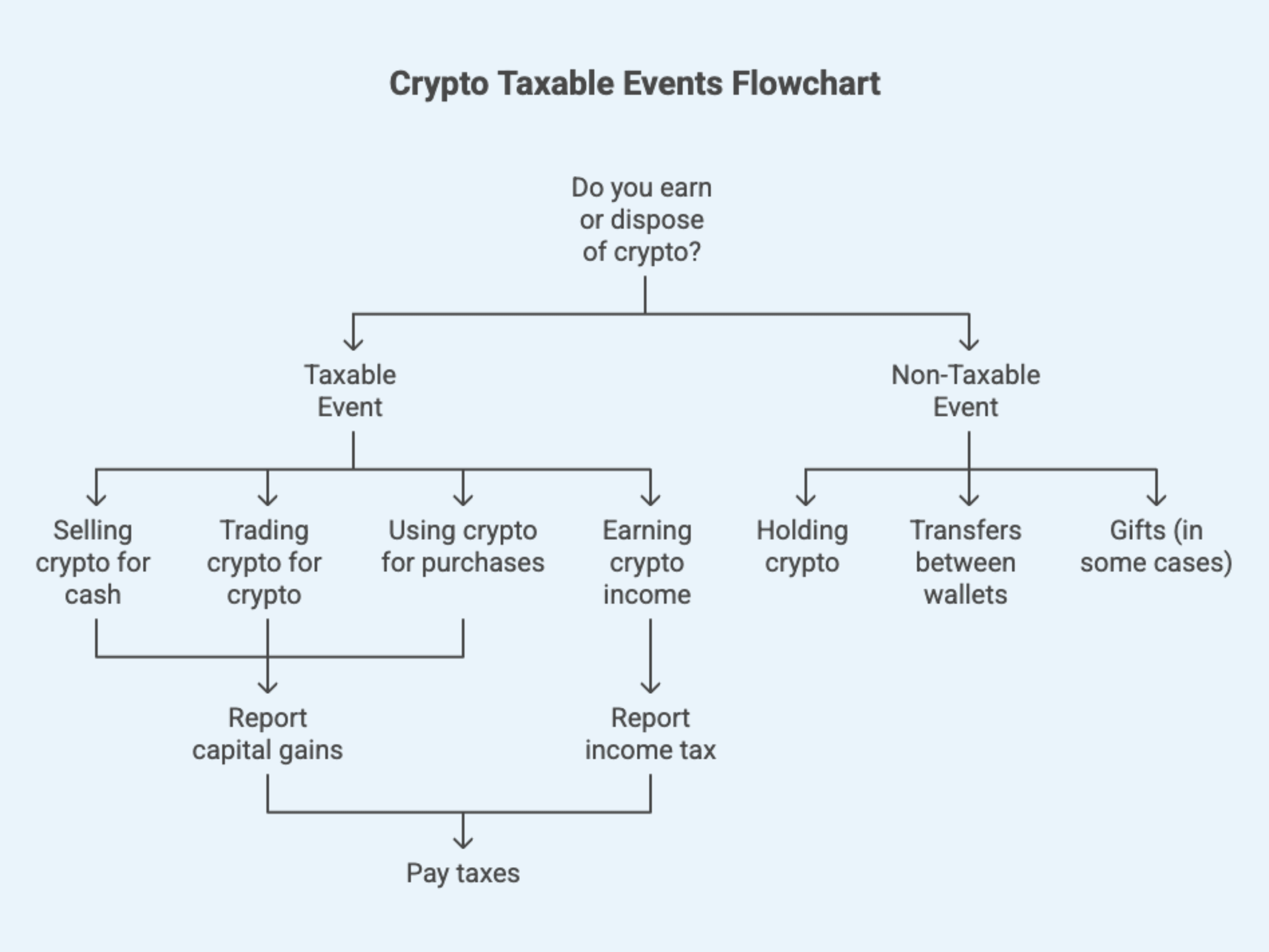

What Counts as a Taxable Event? (The Moments You Owe Tax)

Not everything triggers tax. Here are the main ones, explained simply:

You sell crypto for naira or dollars → Tax on the profit.

You trade one crypto for another (Bitcoin to Ethereum) → Yes, tax! It's like selling the first one and buying the second.

You spend crypto to buy something (like a phone or pay rent) → Tax on the profit at that moment.

You earn crypto: staking rewards, DeFi yield, mining, airdrops, or getting paid in crypto → This is usually treated as income, like salary.

Receiving NFTs or tokens as gifts/rewards in most cases.

What does NOT usually trigger tax right away:

Just buying crypto with money and holding it.

Moving crypto between your own wallets (but keep records anyway).